You must have seen or heard of period houses with windows bricked up for no apparent reason. The architectural abnormality resulted from the Window Tax, a form of taxation introduced in England in 1696.

The window tax, a levy on the number of windows in a building, was introduced by William III as a creative means to tax wealth without imposing a property tax or personal income tax. However, its implications went far beyond its financial intentions, deeply influencing architecture and public health.

In the late 17th century, the window tax was introduced to impose taxes based on signs of visible wealth. Homeowners bricked up their windows as a countermeasure to this invasive tax regime, which judged wealth by the number of windows in residence. Simply put, houses with numerous windows were considered wealthier and were, therefore, taxed more heavily.

Exploring the history of the window tax reveals its transition from a financial measure to a societal trend, significantly altering the very nature of British architectural aesthetics.

The introduction of the window tax in Old England disproportionately affected the wealthy and the middle classes as tax rates escalated.

The financial implications were immediate: homeowners and builders began prioritizing tax evasion over architectural aesthetics and health, significantly altering the design of new and existing structures. However, the tax’s effects worsened as it continued into the 18th and early 19th centuries. Minimalism became the defining feature of the architecture that was once recognized for embracing light and air.

The impact of the window tax was evident in the reduction of windows in new construction and blind windows in existing residences; the effect was not a surface alteration; rather, it represented a change in society’s priorities, with financial concerns now superseding the basic human need for light and air.

Furthermore, the window tax had unintended social consequences, particularly for poor people who lived in smaller properties with fewer windows. This public health issue was so pressing that it led to debates about the tax being a “tax on health,” highlighting the negative impact of the tax policy on personal liberty and public welfare.

Over time, the financial implications of the window tax underwent substantial changes, deeply intertwined with the economic and political landscape of the era.

Initially, the tax consisted of two components: a flat rate charge and a variable tax based on the number of windows above a threshold. This two-tiered system aimed to minimize the tax burden on lower-income households while enforcing a larger tax on wealthier property owners.

As the eighteenth century progressed, the window tax evolved into a more complex system, incorporating a flat rate tax for properties with a certain number of windows. This flat rate was supplemented by additional taxes, mirroring the structure of church rates and other levies of the time, which were also based on the value and size of property holdings.

The window tax system was based on a flat-rate house tax of two shillings per house. After accounting for inflation, it amounted to about £14.76 in 2021 rates. Property owners also had to pay a variable tax based on the number of windows that exceeded a specific limit on top of the baseline price.

10-20 window properties were subject to an additional fee of four shillings, or roughly £29.52 in 2021 currency rates. Furthermore, properties with over twenty windows were subject to an even higher tax burden. Eight additional shillings (about £59.05 in 2021 currency) were charged for these residences.

This additional tax rate reflected that homes with additional windows were wealthier and should thus pay the ‘additional window tax’ into the state treasury.

However, William Pitt the Younger, recognizing the tax’s unpopularity and inefficiency, sought reforms to mitigate its impact, especially on the less wealthy.

Although the window tax had far-reaching implications, it incorporated exemptions intended to soften its impact on specific population segments and certain building types. These exemptions reflect the government’s attempt to balance economic needs with social equity.

A noteworthy category was individuals already exempt from paying church or poor rates due to economic hardship. This provision ensured that the Window Tax did not further burden those who were financially vulnerable. This exemption showed a fair way of taxing people based on what they could afford.

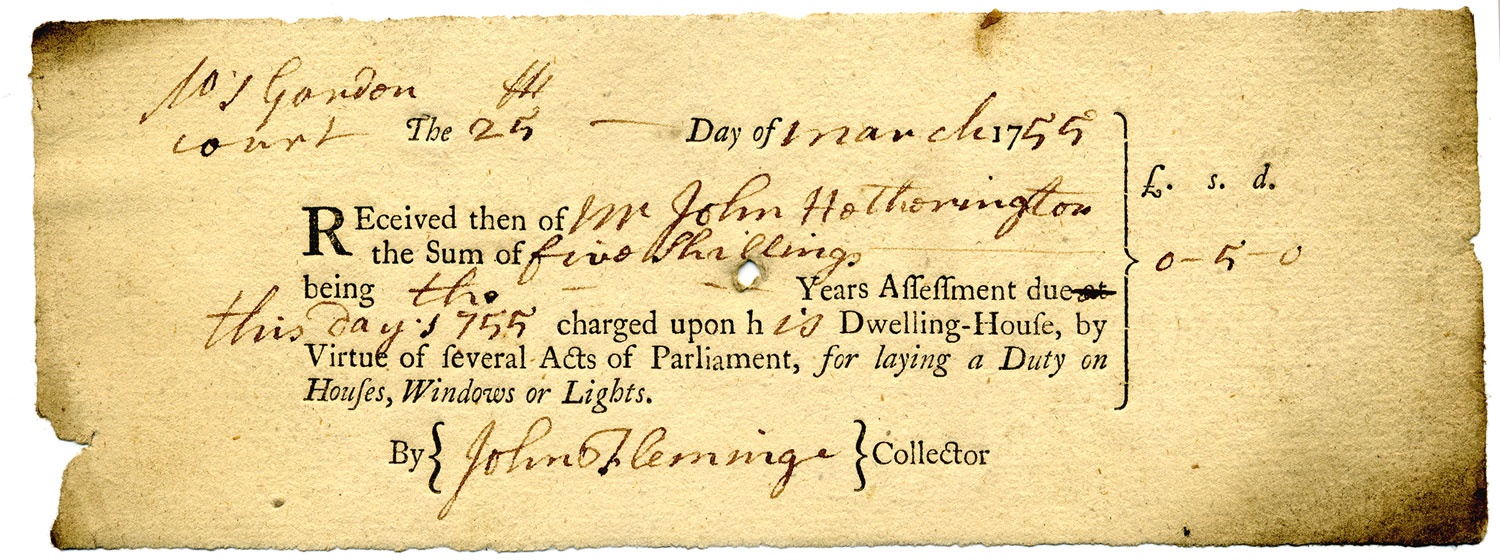

An illustrative case of the tax’s selective application involves the Manchester Royal Infirmary. In 1841, the institution faced a tax obligation of 1/9d (one shilling and nine pence) per window for spaces occupied by its staff, accumulating to a total of £1 9/9d (one pound, nine shillings, and nine pence). This instance highlights the tax’s reach, sparing no sector yet underscoring the slight considerations given to buildings serving critical public functions.

Certain rooms integral to agricultural and food preservation practices, such as dairies, cheese rooms, and milk houses, received exemptions, provided they were marked as such. This exemption recognized the importance of these spaces to rural economies and food production, sparing them from the financial strain that could compromise their operations.

Charles Dickens and other contemporaries criticized the window tax for encouraging social inequalities, using their works to highlight the absurdity and injustice of taxing essential elements like light and air. They saw the tax as an intrusion into private matters, with the government dictating the architectural features of Georgian properties.

This led to the development of the characteristic Georgian windows, designed to maximize light while minimizing tax liability. Property owners, eager to avoid higher taxes without compromising on the aesthetic feature of their homes, often opted for designs that included sufficient light through fewer but larger windows.

The strong agitation against the window tax paved the way for its eventual repeal in 1851. Its end marked a significant victory for advocates of public health, social justice, and economic progress.

The dissolution of the tax made it possible to redesign architecture with a renewed focus on air, light, and aesthetics once again. This period marked a significant shift in British tax policy with the introduction of William Pitt’s idea of income tax as a more equitable alternative.

The move towards the concept of income tax rather than architectural features or property size was seen as a step towards respecting personal liberty and reducing governmental intrusion.

The lasting effects of the window tax are visible today in the bricked-up windows of historic buildings, serving as a reminder of a time when sunlight was taxed.

These architectural remnants tell a story about how window tax altered the appearance of buildings and impacted the well-being of their inhabitants, underscoring the unintended consequences of well-intended policies.